Inflation, Rates & Valuation

Conventional wisdom may or may not apply.

The pandemic generated historic increases in liquidity from the Federal Reserve and an array of stimulus measures.

Supply chain disruptions and irregular demand patterns have created lots of supply/demand imbalances - many have led to strangely high prices. For a time a lowly 8ft 2x4 was selling for $15 at the home improvement center. Residential real estate has surged higher and economists point out that it takes about 5 quarters for that to show up in measured inflation.

There is an argument raging around how “transitional” these price pressures are. Some clearly are. For example, the 2x4 mentioned above has been coming back to earth and is now a little over $5. That’s still about 2x where it was pre-disruption but getting more affordable.

Conventional thinking argues that this is a “big worry” for high valuation stocks because if rates are raised to dampen inflation then valuation multiples will “compress” and stock prices will come down.

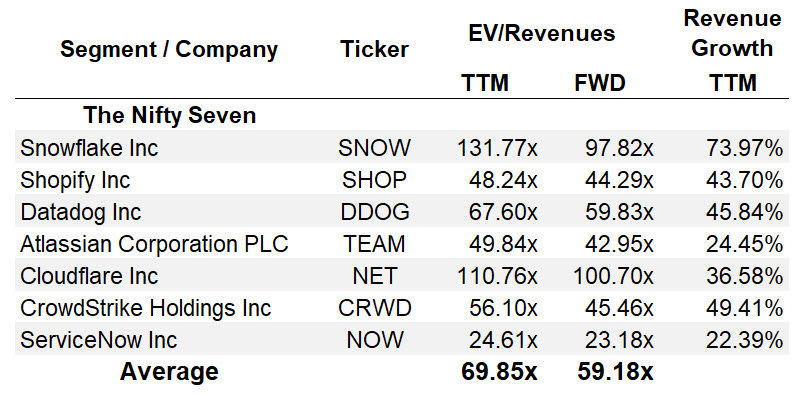

So far there has been plenty of hand-wringing but not much downside in high multiple stocks. For example, take a gander at where some of the “nifty” SaaS names are trading now:

Do not adjust your HP-12C those are the current revenue multiples for this group. They seemed high at 20x, then 40x, and now 60x.

The Ultimate Resource

Supply and demand disruptions create price volatility. But if prices remain elevated human ingenuity and capital get deployed to profit off the new condition. This might not be true for every asset class (think original art) but it works for most.

It’s not just about making more of whatever material has now become dear. Followers of the commodity sector cite management teams that refuse to invest in creating additional capacity no matter how high prices get. That’s an argument for ever-higher prices and fat profits.

But the other side of the equation is demand. Elasticity is part of it. (if gas prices get high enough you drive less or if lumber prices get too high you put off building that new deck you wanted.) Substitutes play a role too and add to the elasticity of demand.

Finally, there is innovation and invention of completely new ways of doing things. Imagine an EV battery without Lithium? Imagine standard roof materials having embedded and cheap solar power harvesting? It doesn’t matter what it is but rather that if the price goes up and stays there we find ways to get it back on a deflationary path.

Valuation and Rates

The theory is that the market discounts future earnings (or future terminal valuations) using a rate that is indexed to risk-free rates.

It may be used in many investment areas but for high-growth technology stocks not as much. The “rule of thumb” back in the 1990’s that 15% was the “correct” discount rate to use. It wasn’t scientific or indexed but it was satisfactory and worked very well at the time.

This sort of approach doesn’t work at all in the “nifty” group. Take Cloudflare (NET) which now trades at over 100x sales. There is no “model” that really gets you to that price even if you apply a 0% discount rate.

The current $66B market value is about 66x 2026G operating earnings. (The G stands for a wild-ass guess.) That’s not terrible but it’s a long way to 2026 and while they may well eat Akamai’s (AKAM) lunch for a few years there are other players that may offer stiffer resistance.

There are some smart people out there on the macro side that say governments have learned that shifting power away from central bankers to governments can give them greater control over interest rates. It’s possible that this strategy will work.

When combined with a long-term persistence about disinflation this might keep rates and valuations at a very high level.

Even if you’re concerned about inflation the only real way to combat it is to own assets, stocks being one example.

As an investor, this is the environment you are currently confronted with. Either you figure out a way to play it or it leaves you behind. I added Rivian (RIVN) to the real-money portfolio last week because it is poised to be an important player in the EV space. I did a form of “valuation” based on their manufacturing capacity and where Tesla (TSLA) is trading. All one can say is that if sentiment for Rivian ends up being comparable to what Tesla has achieved and they execute the next two years, the stock will be substantially above the current price.

As a reminder, everything we write here is purely for entertainment purposes and never constitutes anything else.